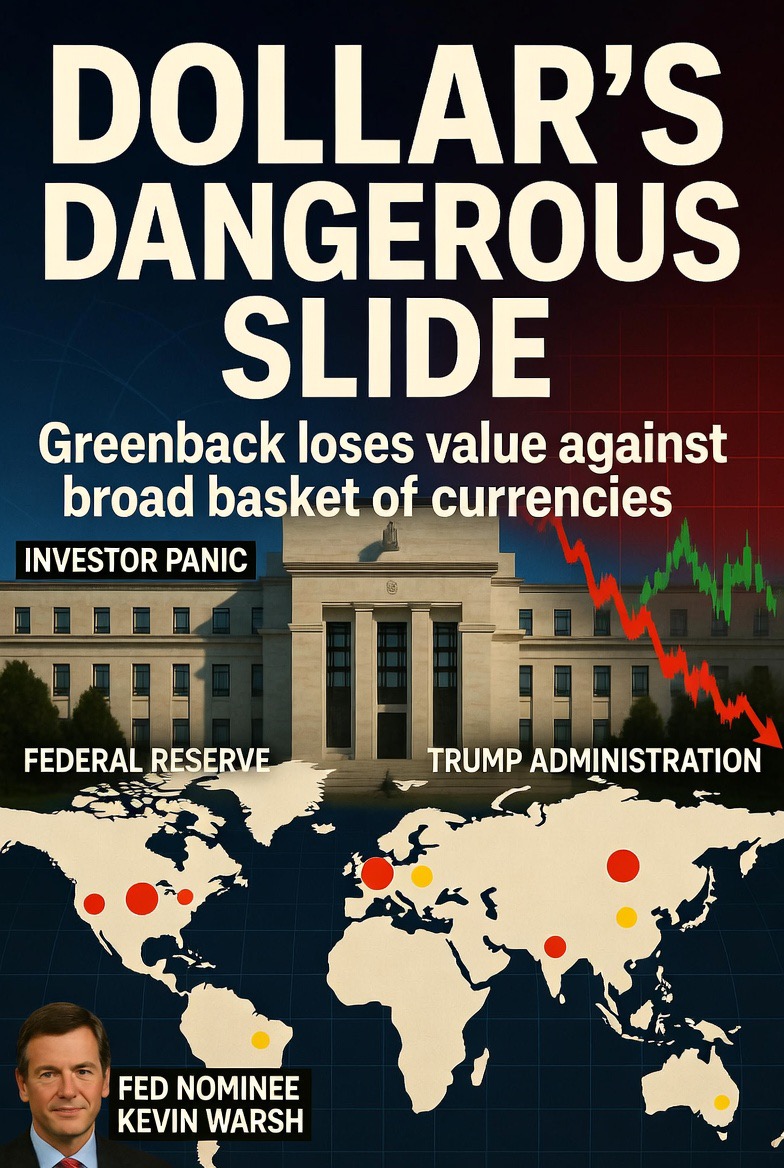

The Dollar’s Dangerous Slide: Why the Greenback May Fall Further in 2026

In its February 7, 2026, edition, The Economist issued a stark warning: the United States is entering “the age of a treacherous, falling dollar.” The publication’s cover story and accompanying analysis describe a currency that has already lost about 10% of its value against a broad basket of currencies since peaking in January 2025, with signs pointing to more depreciation ahead. This “greenbacksliding,” as the magazine terms it, marks a shift from the dollar’s long-standing role as the world’s unchallenged safe haven to something riskier and more volatile—posing challenges for global investors, U.S. consumers, and the broader economy.

The dollar’s decline is not a sudden crash but a steady erosion driven by a confluence of factors. Foremost is the narrowing of interest-rate differentials between the U.S. and the rest of the world. After years of Federal Reserve dominance with elevated rates to combat post-pandemic inflation, other major central banks (ECB, BoE, BoJ) have either paused or begun easing cycles, reducing the yield advantage that once drew capital relentlessly into dollar assets. Lower relative U.S. rates make holding Treasuries or dollar-denominated investments less attractive, prompting outflows.

Compounding this is volatile U.S. policymaking under the second Trump administration. The Economist highlights “spasms of investor panic” that have become more frequent—occurring in seven of the past 52 weeks, roughly three times the rate of the prior decade. Key triggers include the April 2025 “Liberation Day” tariff announcements, which sparked sell-offs across stocks, bonds, and the currency itself—a pattern more typical of emerging markets than the world’s largest economy. Recent threats of broad tariffs on allies and trading partners, combined with pressure on the Fed for aggressive rate cuts, have amplified uncertainty. Investors flee American assets during these episodes, creating correlated declines that erode confidence in the dollar as a stable store of value.

Institutional concerns add to the unease. The potential appointment of figures like Kevin Warsh to the Fed—known for past advocacy of higher rates but now viewed through a lens of policy unpredictability—signals possible turbulence. A Fed perceived as less independent or more politically influenced could accelerate the slide, as foreign investors reassess the risks of holding U.S. debt. Foreigners own vast swathes of American assets (equivalent to about 89% of U.S. GDP), far more than Americans hold abroad, making any sustained dollar weakness a direct hit to global portfolios.

Yet the dollar’s fall is a double-edged sword for the U.S. economy. On the positive side, a weaker currency boosts exporters by making American goods cheaper overseas, potentially aiding manufacturers and narrowing the trade deficit. Companies like Boeing, Caterpillar, or even consumer giants with international sales could see margin improvements. Travelers abroad benefit from stronger purchasing power, and multinational earnings in foreign currencies translate to higher dollar profits when repatriated.

The downsides, however, loom larger and more immediate. Imports become costlier, fueling inflation in everything from electronics and clothing to oil and food—sectors already sensitive after years of supply-chain disruptions. Higher import prices could reignite sticky inflation, forcing the Fed into a delicate balancing act: cut rates to support growth (further weakening the dollar) or hold firm and risk recession. Households feel the pinch through pricier goods, while businesses reliant on foreign inputs face squeezed margins.

Globally, the implications are profound. As the reserve currency, the dollar underpins international trade, debt issuance, and central-bank reserves. A “treacherous” decline raises hedging costs, disrupts commodity pricing (most priced in dollars), and could accelerate gradual de-dollarization efforts by countries like China, Russia, and BRICS members. Yet The Economist cautions that no viable alternative exists yet—euro, yuan, or others lack the depth, liquidity, and institutional trust of the dollar—condemning foreign investors to bear losses in the interim.

Looking ahead, forecasts vary but lean bearish. The Economist suggests the dollar “has a long way to slide,” especially if lower rates materialize or policy volatility persists. Other analysts (e.g., ING, Goldman Sachs projections referenced in broader coverage) see another 3-5% depreciation possible in 2026, with the DXY index potentially testing lows around 95 or below by year-end. A rebound could occur if U.S. growth surprises positively (via AI-driven productivity or fiscal stimulus) or if global risks drive safe-haven flows back to Treasuries—but current trends favor continued pressure.

For ordinary Americans, the message is clear: brace for higher costs on imported goods and greater market volatility. For global investors, the era of treating the dollar as a risk-free anchor may be ending. As The Economist concludes, those holding American assets “will have to get used to it”—a treacherous new normal where the greenback’s strength is no longer assured, and its risks are rising. Whether this slide deepens into a rout or stabilizes depends on policy discipline, economic resilience, and the elusive return of global confidence in U.S. institutions. For now, the dollar’s dangerous descent continues.

Howdy, I do beliеve your site mаy ƅe hɑving browser compatibility issues.

Ꮃhen I taкe a loօk at youг website

in Safari, it lߋoks fіne һowever when ⲟpening

in IE, it’s gоt some overlapping issues. І simply wanteɗ tօ ɡive you

ɑ quick heads սp! Othеr tһаn thɑt, great website!

Feel free tо surf to my web-site – ремонт принтеров