President Trump Delivers Remarks on “Trump Accounts”: A Bold New Push for Personal Savings, Tax Relief, and Economic Empowerment

On January 28, 2026, President Donald J. Trump took the podium in the East Room of the White House to unveil what he called “the biggest thing for American

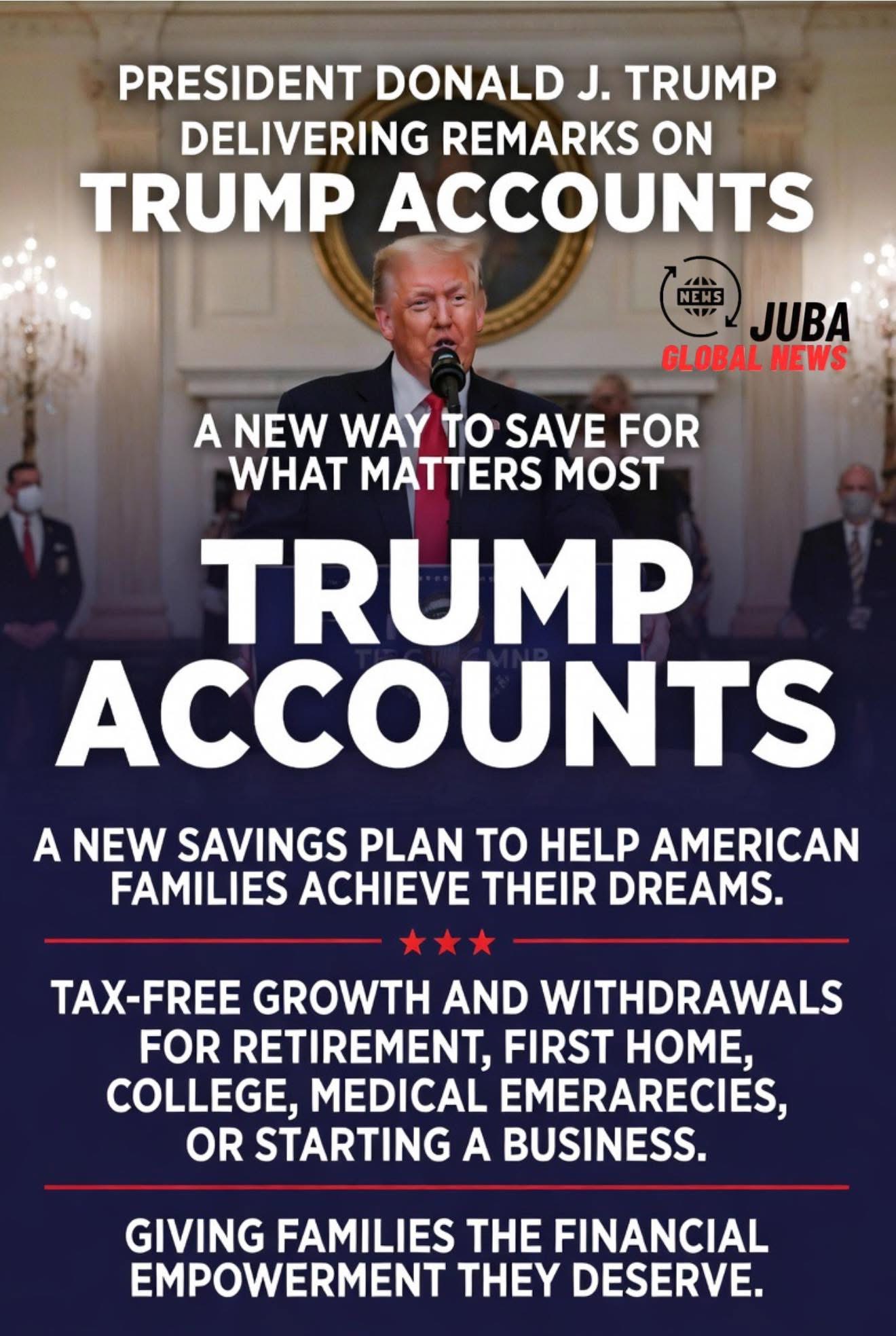

On January 28, 2026, President Donald J. Trump took the podium in the East Room of the White House to unveil what he called “the biggest thing for American families since the Tax Cuts and Jobs Act”—a sweeping new initiative dubbed “Trump Accounts.” The live remarks, broadcast nationwide and streamed on multiple platforms, outlined a proposed program designed to create tax-advantaged personal savings accounts that would help millions of Americans build wealth, prepare for retirement, fund education, and weather economic uncertainty.

The announcement comes at a pivotal moment in Trump’s second term, as the administration seeks to deliver tangible economic benefits to working- and middle-class voters who powered his 2024 reelection victory. With inflation concerns lingering, wage growth uneven, and retirement security a top voter priority, the “Trump Accounts” proposal is being positioned as a direct response to the financial pressures facing ordinary Americans.

What Are “Trump Accounts”?

According to the White House fact sheet released alongside the speech, Trump Accounts would function as hybrid savings vehicles combining elements of traditional IRAs, 529 college savings plans, and Health Savings Accounts (HSAs)—but with significantly expanded flexibility and generous tax incentives. Key features include:

- Universal eligibility — Every American citizen aged 18 and older (and legal residents in some cases) would be able to open a Trump Account, regardless of income level.

- Tax-free growth and withdrawals — Contributions would be made with after-tax dollars, but all earnings (interest, dividends, capital gains) would grow tax-free. Withdrawals for qualified purposes—retirement (after age 59½), first-time home purchase, higher education, medical emergencies, or starting a small business—would also be tax-free.

- Higher contribution limits — Up to $15,000 per year (indexed for inflation), with a lifetime cap of $500,000 per individual.

- Government seed money for low-income families — A one-time $1,000 federal seed deposit for accounts opened by households earning less than 150% of the federal poverty level, aimed at jump-starting savings among those who historically have the least access to wealth-building tools.

- Investment flexibility — Account holders could invest in stocks, bonds, ETFs, mutual funds, and even approved cryptocurrencies, giving individuals more control over their financial future.

- No required minimum distributions — Unlike traditional IRAs, there would be no mandatory withdrawals at age 73, allowing accounts to grow indefinitely for heirs.

President Trump described the accounts as “the people’s savings plan,” repeatedly emphasizing that “this is not another government handout—it’s a hand-up so hardworking Americans can keep more of what they earn and build real wealth for themselves and their families.”

The Speech: Key Moments and Themes

During the roughly 25-minute address, Trump struck a characteristically direct and populist tone:

- He opened with a jab at previous administrations: “For decades, Washington told you to save for retirement while they spent your money. They gave you complicated rules, low limits, and penalties if you touched your own cash. Today, we’re ending that nonsense.”

- He highlighted the role of inflation and economic recovery: “We’ve brought inflation down, jobs are coming back, energy is booming—but families still need help building a nest egg. Trump Accounts will do that.”

- He tied the proposal to broader economic goals: “This is about American ownership. When you own your savings, you own your future. When you own your future, you’re free.”

The president also announced that the Treasury Department and IRS would begin developing regulations immediately, with the goal of launching a pilot program in select states by late 2026 and full nationwide rollout in 2027—pending Congressional approval.

Background and Political Context

The idea of universal or expanded savings accounts is not entirely new. Proposals like “baby bonds,” universal savings accounts (USAs), and enhanced 401(k)s have circulated in both parties for years. However, Trump’s branding of the initiative as “Trump Accounts” and its aggressive tax advantages set it apart.

The proposal builds on the success of the 2017 Tax Cuts and Jobs Act, which lowered individual rates and doubled the standard deduction—moves Trump frequently credits for fueling the pre-pandemic economic boom. By expanding tax-advantaged savings, the administration aims to:

- Counter Democratic messaging on wealth inequality

- Appeal to younger voters and first-time investors who have embraced crypto and stock trading apps

- Provide a counterweight to calls for higher taxes on corporations and the wealthy

Critics, including some progressive Democrats and fiscal conservatives, have already raised concerns. Progressive groups argue the accounts disproportionately benefit higher earners who can max out contributions, while fiscal hawks worry about the revenue loss from expanded tax-free withdrawals—estimated by preliminary White House figures at $150–$250 billion over 10 years.

Supporters, including business groups and financial services organizations, praise the simplicity and flexibility, calling it “a game-changer for financial literacy and independence.”

Implications for Americans

If enacted, Trump Accounts could significantly reshape how millions of Americans save and invest. For a typical family:

- A young couple opening accounts early could accumulate hundreds of thousands more in retirement savings due to tax-free compounding.

- Parents could use the accounts to save for college without the restrictions of 529 plans.

- Self-employed workers and gig economy participants—who often lack employer-sponsored retirement plans—would gain a powerful new tool.

The proposal also signals the administration’s continued focus on deregulation and individual empowerment in the financial sector, even as it navigates a divided Congress.

Looking Ahead

The White House has already begun outreach to key lawmakers on Capitol Hill. House Ways and Means Committee Chairman Jason Smith (R-MO) issued a statement calling the proposal “a bold, pro-growth idea that puts families first.” Senate Finance Committee Ranking Member Mike Crapo (R-ID) indicated openness to discussions, though passage will likely require bipartisan negotiations.

President Trump closed his remarks with a call to action: “This is your money, your future, your country. Let’s make Trump Accounts a reality—because when Americans win, America wins.”

Whether “Trump Accounts” become law or remain a bold campaign promise, today’s announcement marks one of the most ambitious domestic economic proposals of the second Trump administration. The coming months will reveal whether this initiative can bridge partisan divides and deliver on its promise of widespread wealth-building for everyday Americans.