Asian Stocks Climb to Six-Week High Amid Year-End Optimism and Thin Holiday Trading

December 26, 2025 – In a subdued yet upbeat session marking the post-Christmas trading day, Asian stock markets advanced to their highest levels in six wee

December 26, 2025 – In a subdued yet upbeat session marking the post-Christmas trading day, Asian stock markets advanced to their highest levels in six weeks, extending a late-year rally driven by renewed risk appetite, expectations for further monetary easing, and a weakening U.S. dollar. With many global exchanges closed for Boxing Day—including Australia, Hong Kong, and much of Europe—trading volumes remained exceptionally thin, amplifying moves in open markets like Japan, South Korea, and mainland China.

The MSCI Asia-Pacific ex-Japan index rose for a sixth consecutive session, reaching its peak since mid-November. This performance capped a remarkable 2025 for regional equities, with several benchmarks posting their strongest annual gains in years amid recovering economies and supportive policies.

Standout Performers: Japan and South Korea Lead the Charge

Japan’s markets shone brightly. The Topix index climbed 0.5% to a fresh all-time record, reflecting broad-based strength in domestic shares. Tech giants like SoftBank Group surged over 2%, while semiconductor-related firms such as Advantest and Lasertec posted solid gains. The broader Nikkei 225 advanced around 0.7%, buoyed by a softer yen that enhanced export competitiveness.

South Korea’s KOSPI index rose 0.6%, pushing its year-to-date gain to an impressive 72%—making it the world’s best-performing major stock market in 2025. This extraordinary run has been fueled by robust semiconductor demand, corporate governance reforms, and heavy foreign inflows into tech heavyweights.

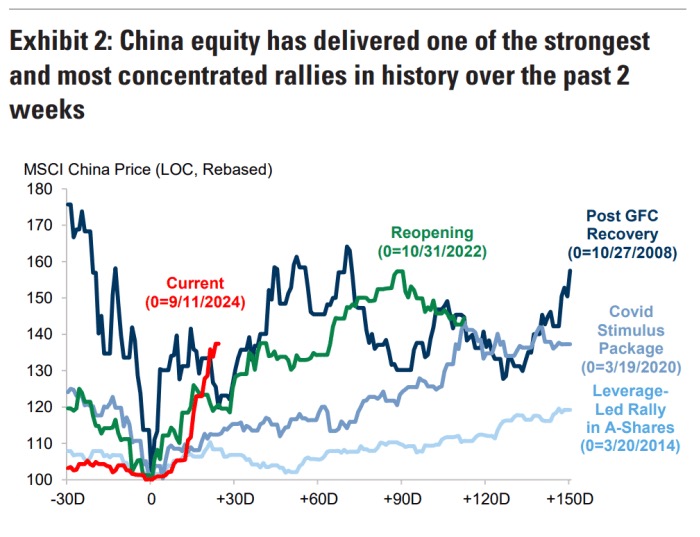

On the mainland, China’s CSI 300 blue-chip index edged up 0.27%, on track for an 18% annual increase—its strongest since 2020—supported by stimulus measures and improving economic indicators. 1

Drivers Behind the Rally

Several interconnected factors underpinned the upward momentum:

- Year-End Risk Appetite: Investors are positioning for a classic “Santa Claus rally,” with optimism around global growth and policy support encouraging dips-buying in thin liquidity.

- Currency Dynamics: The U.S. dollar index hovered near multi-month lows, down 0.8% for the week—its weakest since July. A softer dollar makes Asian exports more competitive and attracts capital flows into emerging markets. The yen’s depreciation, despite recent Bank of Japan rate hikes, kept intervention risks alive but supported Japanese equities.

- Monetary Policy Expectations: Markets are pricing in further Federal Reserve rate cuts in 2026, reducing the appeal of cash holdings and boosting risk assets. Uncertainty surrounds President Trump’s upcoming nomination for Fed chair, but dovish signals dominate sentiment.

- Bond Market Relief in Japan: Japanese government bond yields eased from 26-year highs after Prime Minister Sanae Takaichi reassured markets on fiscal restraint, stabilizing fixed-income sentiment.

- Broader Commodity Tailwinds: Parallel surges in precious metals—silver topping records and gold nearing $4,500—signaled investor rotation into hard assets amid lingering geopolitical concerns.

Challenges and Thin Liquidity Warnings

Despite the gains, analysts cautioned that low volumes—exacerbated by holiday closures—could exaggerate price swings. “This is classic year-end window dressing,” noted one Singapore-based strategist. “Real conviction will return in January with fresh catalysts like earnings and policy updates.”

Geopolitical tensions and potential U.S. policy shifts under the incoming administration remain wildcard risks for 2026.

Outlook into 2026

As 2025 draws to a close, Asian equities have outperformed many peers, benefiting from regional recovery themes and undervaluations relative to U.S. megacaps. South Korea’s dominance highlights the semiconductor supercycle, while Japan’s records underscore corporate reforms and BOJ normalization.

With global indices at or near highs, the stage is set for continued volatility—but the underlying tone remains constructive, provided central banks maintain accommodative stances.

This quiet Boxing Day session encapsulated 2025’s resilient equity story: thin trade, but unmistakable year-end optimism shining through.